Click here for a printer-friendly version of this document.

What is crop insurance?

Much like your car insurance limits the financial loss you incur when something bad happens to your vehicle, crop insurance serves to limit financial loss when your farm experiences declines in production or revenue. Over the long term, crop insurance should reduce farm income volatility.

How does crop insurance work?

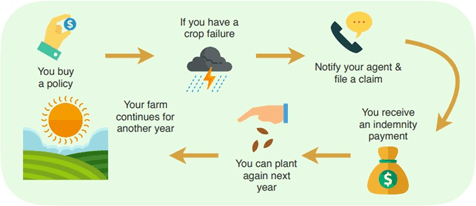

As is often the case with other types of insurance, you purchase a policy covering an agreed-upon liability. If you incur a loss due to a covered cause of loss, you can file a claim with your insurance provider and you will receive an indemnity payment to make you “more whole”.

What types of crop insurance are available?

There are currently several types of federal crop insurance products available. These products function differently and protect against different types of risk.

- Yield Products – Cover individual crop yield losses that cause production to fall below a farm’s historical production levels.

- Dollar Plan – Loss payment based on expected value of the crop, relative to the dollar amount of insurance.

- LGM – Livestock Gross Margin makes a payment when your gross margin falls below the guaranteed gross margin.

- PRF – Pasture Rangeland and Forage makes an automatic payment based on your coverage level when rainfall or snowfall in your area (grid) falls below historical averages

- Revenue Products – Cover revenue losses due to individual crop yield losses and price decreases.

- WFRP – Whole Farm Revenue Protection covers losses to the entire farm’s expected revenue.

Crop insurance products on the market include both private and federal policies…

Private crop insurance – Private insurance companies offer private insurance policies, which typically only cover losses caused by a single specific peril (e.g., hail crop insurance, which pays an indemnity on only losses incurred from a hail event). Private crop insurance premiums are unsubsidized and set by the insurer, as are indemnity levels. The costs of selling the policy, premium revenues, and underwriting gains are all borne by the companies selling the policy.

Federal crop insurance – Federal crop insurance is administered through the USDA – Risk Management Agency (RMA) in partnership with approved private insurers (AIPs). The AIPs market this insurance through a network of licensed agents. Many of these policies are multi- peril crop insurance (MPCI) policies, which means they cover losses caused by a variety of perils. Premiums are set by the RMA and are federally mandated to be actuarially fair – meaning that the premiums must be equal to the value of the expected indemnity, with no additional loading for selling costs or revenue. Premium costs for federal crop insurance policies will not vary across different insurance providers: providers can only differentiate themselves through the service they provide. Additionally, premium costs for federal crop insurance are shared by the federal government so a producer does not have to cover the total cost of the crop insurance premium. USDA provides a payment to AIPs to cover selling costs and shares in underwriting gains or losses with the AIPs.

What about crop insurance for hemp?

Currently hemp is not covered by any federal crop insurance policy. However, the USDA recognizes the importance of providing an effective safety-net to reduce some of the uncertainty faced by those adopting this new crop. The RMA is forming focus groups to tackle the issue and there is speculation that the development of single-crop insurance policies for hemp will begin in the near future, but these policies are unlikely to be made available for at least a few years. A likely first step towards providing a robust suite of hemp crop insurance products is the addition of hemp to the “approved commodity list” of the Whole Farm Revenue Protection (WFRP) crop insurance policy.

In the meantime, it is important for those in the industry to remain vocal about their need for effective off-farm risk management solutions and to work closely with their university extension to expedite the development of crop insurance for hemp.

For more NY crop insurance information, visit: www.agriskmanagement.cornell.edu